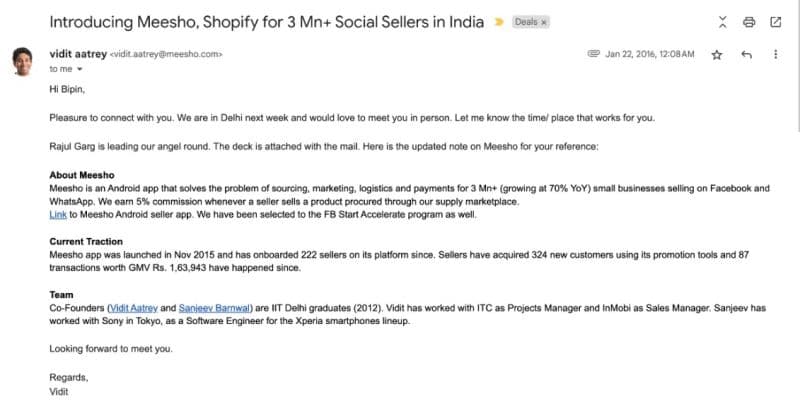

An early investor’s inbox snapshot is capturing the scale of Meesho’s journey from scrappy seed‑stage startup to public‑market debutant. In January 2016, a young Vidit Aatrey mailed the investor with the subject line “Introducing Meesho, Shopify for 3 Mn+ Social Sellers in India,” pitching an Android app that helped small businesses on Facebook and WhatsApp manage sourcing, marketing, logistics and payments, and charged a 5% commission on each sale routed through its marketplace.

In that mail, Aatrey noted that Meesho had been launched just a few months earlier in November 2015, had onboarded 222 sellers, brought them 324 new customers, and processed 87 transactions with a GMV of about ₹1.63 lakh, while also highlighting that the company had entered the Facebook Start Accelerator programme.

The investor, who now calls it a “10‑crore valuation entry opportunity,” says he had to pass at the time because backing Meesho conflicted with the main group business at his then VC firm. Looking back as Meesho heads to the public markets at around a ₹50,000‑crore valuation, he describes the company as a “bombastic success,” congratulates Aatrey and cofounder Sanjeev Barnwal, and gives a shout‑out to Elevation Capital, Peak XV Partners and WestBridge Capital for staying the course. The tone of the post mixes FOMO and admiration: “I missed it – not Zhakaas. But overall Zhakaas,” he writes, framing it as a big win for “Bharat‑first” entrepreneurship.

Meesho’s IPO blueprint

Meesho’s red herring prospectus lays out one of the most closely watched tech listings of 2025. The Bengaluru‑based ecommerce company is raising ₹4,250 crore via a fresh issue, paired with an offer for sale of 10.55 crore shares from existing investors and founders. The price band has been set at ₹105–₹111 per share, implying a market capitalisation in the ₹47,000–₹52,000‑crore range (about $5.6 billion at the top end).

The issue opens for subscription from 3–5 December, with the anchor book scheduled for 2 December, and the shares are slated to list on both BSE and NSE. Founders Vidit Aatrey and Sanjeev Barnwal are each selling up to 1.6 crore shares in the OFS, while early backers Elevation Capital, Peak XV Partners, Prosus, Venture Highway, Y Combinator Continuity and others are trimming stakes but remain significant shareholders post‑listing.

Use of proceeds is heavily tilted toward technology and growth: about ₹1,390 crore for cloud infrastructure via subsidiary Meesho Technologies, ₹480 crore for salaries of AI/ML and engineering teams, roughly ₹1,020 crore for marketing and brand building, and the balance for inorganic opportunities and general corporate purposes. The message to public investors is that Meesho wants to consolidate its position as a low‑cost, AI‑driven marketplace for value‑seeking consumers and long‑tail sellers.

Read this: Why Is Meesho Skipping Rs 280 Crore in Profit This Year? Founder Explains in Latest Interview Ahead of IPO

Financials: scaling fast, cutting losses sharply

Meesho’s numbers show a rare combination of rapid growth and a steep improvement in profitability:

- H1 FY26: Revenue from operations of ₹5,577.5 crore, up 29.4% year on year from ₹4,311.2 crore in H1 FY25; net loss narrowed to ₹700.7 crore, a 72% reduction versus the ₹2,512.8‑crore loss a year earlier.

- FY25: Revenue from operations of about ₹9,390 crore, up roughly 23% over FY24, with loss before tax shrinking from around ₹1,672 crore in FY23 to just over ₹100 crore in FY25, aided by disciplined discounting and cost control.

- Cash flows: Including interest income, Meesho reported positive free cash flow of roughly ₹1,000 crore in FY25, signalling that the business is no longer dependent on heavy external funding for day‑to‑day operations.

The RHP also discloses a ₹572‑crore direct tax demand from the Income Tax Department for AY 2022–23, which Meesho has challenged in the Karnataka High Court; the court has granted an interim stay and the matter is pending. This tax overhang is one of the key risk factors flagged for IPO investors.

Operationally, Meesho has pivoted from a pure social‑commerce, reseller‑driven model to a low‑price horizontal marketplace, with a strong tilt toward fashion, beauty and home categories in Tier‑II/III India. Investments in AI‑driven cataloguing, recommendation engines and logistics optimisation have helped it lower customer‑acquisition costs and improve delivery reliability, which is where a substantial slice of the IPO money will go.

In the public‑market narrative, this trajectory—from a 2016 seed‑stage email about 222 sellers and ₹1.6‑lakh GMV to a ₹50,000‑crore IPO with double‑digit revenue growth and rapidly shrinking losses—is what makes the “missed at 10 crore” anecdote so striking. It encapsulates how quickly Indian consumer internet winners can compound when the founder‑market fit, timing and execution align—and why even seasoned investors sometimes look back at an old inbox screenshot and say, only half‑jokingly, that their decision was “not Zhakaas” after all.

{kind=link}